"Nationally, 58% of flats, units and apartments are owned by investors. That is quite an amazing statistic, especially when you compare that with detached houses where only 21% are investor owned.

Across the capital cities the proportions are even higher. Darwin tops the list with 70.6% of all units being rented followed by Brisbane where 70.2% of all units are rented."

See RP Data Blog

Friday, August 3, 2012

Barefoot Investors Advice re Property

"My

opinion on traditional Aussie housing hasn't changed one iota: I still

firmly believe that most investment properties bought today are a trap.

Their prices are too high and their returns too low to justify the

dangerous debt burden needed to 'get in the property game'.

That

fact is backed up by the Australian Tax Office's latest figures, which

show that, despite collecting $28 billion in rents last year,

Australia's landlords still reported a $4.8 billion loss. Less than four

in ten property investors made any money last year."

Source: Barefoot Investor

Thursday, August 2, 2012

South Brisbane apartment

Proposed apartment building by Aria at 77 Grey Street in South Brisbane. Proposed to be 18 stories.

36 two bedroom apartments & 84 one bedroom apartments (for a total of 120 apartments), but only 106 car parks including visitor car parking.

Many of the apartments will have a nice view of the wall of the museum, or the very busy Grey St/Melbourne St intersection and busway.

36 two bedroom apartments & 84 one bedroom apartments (for a total of 120 apartments), but only 106 car parks including visitor car parking.

Many of the apartments will have a nice view of the wall of the museum, or the very busy Grey St/Melbourne St intersection and busway.

Queen Street Proposal

Proposed building by Grocon for the failed Trilogy site in Queen Street. Aurora Towers on the far left. The proposed building is not riverfront, but on the far side of the road from the river. Newspaper reports say that national law firm Freehills has agreed to rent the top 3 floors. I wonder if this building will get off the ground, or be like Trilogy Tower and never be built?

Gold Coast Prices Have Further to Fall

THE Gold Coast housing market is about six months off the bottom, according to analysts. Two separate housing indexes showed a rise in capital city house values in June, indicating the slump in house prices appears to have bottomed and the market is about to improve again, underpinned by recent interest rate cuts.

But the Gold Coast recorded one of the largest falls of any region in the country and still has some way to go, according to RP Data research director Tim Lawless. "I don't think it has reached the bottom yet but the Gold Coast is probably approaching that mark and in the next six months should bottom out and start turning around," he said.

Story Here

But the Gold Coast recorded one of the largest falls of any region in the country and still has some way to go, according to RP Data research director Tim Lawless. "I don't think it has reached the bottom yet but the Gold Coast is probably approaching that mark and in the next six months should bottom out and start turning around," he said.

Story Here

111 Eagle St Opening

111 Eagle Street opened last night. It is not an apartment building, but it is next door to Riparian apartments. Photo here.

No significant improvement: RP Data

Summary of RP Data report:

Capital city home values increased by 0.6% in July after increasing by 1.0% in June

·

Capital city dwelling values increased by 0.6% over

the month of July 2012. Dwelling values are down -0.6% over the first

seven months of 2012 and down -2.4% over the twelve months to July 2012. Home values remain -5.9% below their historic highs

across the combined capitals with falls from the peak ranging from

-11.5% in Brisbane to -2.9% in Sydney.

· Looking at value movements across broad price segments in the market to June 2012, the premium housing market is recording the largest falls (down -3.4% over the year) while the broad ‘middle market’ has been the most resilient with values falling by -2.0% and the most affordable suburbs have recorded value falls of -2.9%.

· Looking at value movements across broad price segments in the market to June 2012, the premium housing market is recording the largest falls (down -3.4% over the year) while the broad ‘middle market’ has been the most resilient with values falling by -2.0% and the most affordable suburbs have recorded value falls of -2.9%.

Sales activity showed a slight improvement in

May however, there has been no significant improvement to date despite

recent interest rate cuts

·

Estimated sales volumes are currently -14% below

the five year average nationally and -13% lower across the combined

capital cities

·

Compared to volumes in May 2011, sales volumes are currently -4% lower nationally and across the capital cities.

Rents continue to improve in certain areas and across specific product types while yields continue to trend upwards

·

Capital city house and rents have increased by 3.0% over the 12 months to July 2012

·

Gross rental yields for houses have improved from

4.0% last July to 4.2% currently and for units they have increased to

4.9% from 4.6% last year.

Vendor discount levels and time on market are trending lower but remain at elevated levels

·

Based on private treaty sales, it took an average

of 60 days to sell a house in the capital cities in June 2012 compared

to 68 days at the same time last year.

·

Vendors are now providing an average discount of

-7.2% from their initial listings price, at the same time last year the

average vendor discount across the capital cities was recorded at -7.6%

The number of homes for sale has been easing however, on an historical basis they remain at quite high levels

·

RP Data is tracking around 296,000 unique houses

and units that are available for sale across Australia; that’s about 9%

higher than at the same time last year.

·

New listings are actually -14% lower than at the same time last year.

·

More than half of the total listings are located in the non capital city markets despite the fact that only 35% of sales take place in these locations.

Economic data flows remain mixed

·

Headline inflation is at 1.2% and core inflation is at 2.0% and trending lower.

·

The Australian economy grew by 4.3% over the first quarter of 2012.

·

The unemployment rate increased from 5.1% in May to 5.2% in June.

·

Consumer confidence for July 2012 showed that

optimism was outweighed by pessimism however, the Index increased by

3.7% over the month.

·

First home buyers accounted for 17.8% of all owner occupier finance commitments over the month.

·

Overall housing finance (ex-refi’s) are up 2.8% over the year while refinance commitments are up 7.5% over the year.

·

Private sector housing credit continues to grow at record low levels of just 5.1% over the 12 months to June 2012.

·

Dwelling approvals were up 10.2% in June 2012 compared to volumes a year earlier.

Wednesday, August 1, 2012

Brisbane Apartments are Worst Performing Market: RP Data Statistics

Dwelling values across capital cities recorded a second month of capital gains in July with dwelling values up by 0.6% over the month following a 1.0% rise in June. The RP Data-Rismark Home Value indices posted a second successive rise in capital city dwelling values over the month of July. Across the combined capital cities, dwelling values rose by 0.6 per cent over the month with the rises being relatively consistently over the first three weeks of July followed by a -0.2 per cent fall over the final week of the month. Over the three months to the end of July, capital city dwellings have posted an increase of 0.2 per cent.

See RP Data July Release

Brisbane apartment prices:

July 2012 - down 2%

Quarter - up 0.3%

Year to Date - down 3.9%

Year on Year - down 5%

Median price based on settled sales of Brisbane apartments over the quarter - $366,000.

The Brisbane apartment market is the worst performing capital city apartment market in Australia this year.

Below is a chart for dwellings, which includes both houses and apartments:

See RP Data July Release

Brisbane apartment prices:

July 2012 - down 2%

Quarter - up 0.3%

Year to Date - down 3.9%

Year on Year - down 5%

Median price based on settled sales of Brisbane apartments over the quarter - $366,000.

The Brisbane apartment market is the worst performing capital city apartment market in Australia this year.

Below is a chart for dwellings, which includes both houses and apartments:

Brisbane Downtown Ghost town

An interesting article from The Telegraph that says that the Brisbane downtown is a ghost town. But despite this, car parks are charging $72 to park for 3 hours.

Monday, July 30, 2012

Value Accumulation by major Queensland regions

Across Queensland, 9.6 percent of homes are worth less than or equal to their initial purchase price while

36.6 percent of homes are worth more than double their initial purchase price. At the end of the

corresponding quarter in 2011, 3.7 percent of homes were worth less than or equal to their initial purchase

price and 40.3 percent of homes were worth more than double. These results highlight the growing impact

of the continued underperformance of the Queensland housing market.

Source: RP Data

Source: RP Data

Sunday, July 29, 2012

Profits and Losses on Actual Sales Data

From a report from RP Data, that shows a number of people made losses when sell property -- it is not true to say "as safe as houses" if you buy badly or at the wrong time or hold for a short period:

As a special feature in this report we examine the level of gross profit or loss based on residential dwellings that sold during the March quarter of 2012. The results are shown in the graphs below across all sales and also divided between homes that were purchased pre and post GFC (before or after January 1, 2008).

Of those owners that had purchased their home prior to the financial crisis (for the purposes of analysis we have used the date of January 1, 2008), a lower 7.2 percent had sold their home at a loss. A much greater 42.3 percent of these vendors sold their home at price which was at least double the previous purchase price.

Capital gains were much weaker for those vendors who had purchased their home in 2008 or thereafter. A larger proportion of these vendors recorded a loss on their sale, with 27.5 percent of dwellings sold recording a sale price lower than the initial purchase price. On the other hand, only 7.5 percent recorded a capital gain of more than 50 percent compared to the original purchase price. These results reflect the significantly weaker housing market conditions since 2008 and the benefits of a long term hold when it comes to turning a profit on residential property.

As a special feature in this report we examine the level of gross profit or loss based on residential dwellings that sold during the March quarter of 2012. The results are shown in the graphs below across all sales and also divided between homes that were purchased pre and post GFC (before or after January 1, 2008).

Of those owners that had purchased their home prior to the financial crisis (for the purposes of analysis we have used the date of January 1, 2008), a lower 7.2 percent had sold their home at a loss. A much greater 42.3 percent of these vendors sold their home at price which was at least double the previous purchase price.

Capital gains were much weaker for those vendors who had purchased their home in 2008 or thereafter. A larger proportion of these vendors recorded a loss on their sale, with 27.5 percent of dwellings sold recording a sale price lower than the initial purchase price. On the other hand, only 7.5 percent recorded a capital gain of more than 50 percent compared to the original purchase price. These results reflect the significantly weaker housing market conditions since 2008 and the benefits of a long term hold when it comes to turning a profit on residential property.

Thursday, July 26, 2012

Pets - from a reader

We’re big fans of your blog over at Insurancequotes.org and wanted to share with you one of our new favorite posts, about pet and home renting, called, 8 Risks of Renting with a Pet. Your readers might also be interested in taking a look, and we’d appreciate it if you have the space to mention or feature it alongside your regular posts.

Wednesday, July 25, 2012

Comparing Different Apartments

This note came from a real estate agent's newsletter (HS Brisbane Property):

Be informed!!

This is, funnily, exactly what's

happening in the Brisbane CBD with some reported and advertised property sales'

prices - they are both CBD apartments, they both have 2bedrooms, so should they

sell for the same price? Absolutely not. They may have different numbers of

bathrooms, different views, different numbers of car spaces ... and more.

So when I

read 'Highest achieved price for 2bed unit in building 'XYZ' in 3

years!', I think "Hmmm ... could be that they're comparing apples

with tomatoes!".

Without going into details it's

interesting to note:

à An additional car space

will add approx. $60,000 (or in some cases more) to the price of an apartment.

However, a tandem car space will not achieve the same price as a single

carspace. Example: 2bed unit with 2 car spaces will sell for approx. $60,000

more than one with only 1 carspace.

à Views mean $$$

... sometimes. Apart from the direct riverfront views of some buildings and the

eagle-soaring views from the top of 74-floor Soleil or 69-floor Aurora

à Apartment size and no. bathrooms. For a 2bed apartment, 2bathrooms would normally achieve higher prices

than 1bathroom, but this may also depend on other factors such as the overall

apartment size. A larger, well-designed apartment would also be expected to

sell for more than a smaller type. Compare the apartment sizes and floorplans.

Back to our advertised highest

price. Always ask yourself : what types of

apartment is this being compared to? What size, floorplan, level,

outlook, no. bathrooms and carspaces, and what does it include?

It may still be the highest price in

years, but it may be like comparing apples and tomatoes .. they are very

different.

Reader's Comment - Is there a boom?

A reader's view:

There seems to be a dramatic marketing shift going on in Brisbane at present in regard to marketing of apartments and units. The advertising has shifted to promoting the merits of “investing in apartments for rental return” rather than marketing to owner-occupiers. It appears the owner-occupier buyers have all dried up, perhaps they are among the 20,000 workers slated by the State Government for redundancies?

Or are potential owner-occupiers waiting for the release onto the market of thousands of houses and flats currently owned by State and Federal Government that are soon to be placed on the market as a result of the Government push for the private sector to provide (former) public housing by offering the tax-deduction carrot being offered to owners who place rental properties into the NRAS scheme?

One only has to attend the Home Show in Brisbane to see this over-night marketing shift or take a cursory glance at this Saturday’s Courier Mail Property insert. The marketing hype seems to have abandoned the (now) non-existent new owner-occupier buyers and switched to promoting the merits of “investing in units or apartments for rental return” since clearly, the notion of capital gain is now just a pipe dream, at least for the next 5-10 years.

Accompanying press releases and advertisements say how successful the developments are (or going to be – many haven’t even started building) and advertise the numerous sales that have already been made to “investors” for fabulous rental returns. Who is buying these apartments is the question. For example, one in Milton advertises that it has sold $90 million in pre-sales with a vacancy rate of 0.7% and a rental return of 12.4% p.a (Courier Mail Sat 21/7/2012) yet not a sod has been turned on the vacant site. Puzzling indeed.

Others are advertising rental returns of $600-$850 per week around Newstead and Bowen Hills yet a newly completed complex at Bowen Hills, just 2 minutes from the CBD has huge placards visible from the ICB offering rentals at $300 per week. Quite a difference from the advertised rentals of $600-$800 per week available to “investors” less than a kilometre away. Recent data shows around 130 apartments available for lease or sale in the Teneriffe and Newstead area. So while alleged hundreds of units are being “snapped up” by savvy investors cashing in on the “rental boom” (remember the mining boom?) around Brisbane, a number of large unit and/or apartment complexes have been abandoned before they even turned a sod. Puzzling indeed? Yet the marketers claim buyers are scrambling to line up and buy off the plan? More puzzling.

There seems to be a dramatic marketing shift going on in Brisbane at present in regard to marketing of apartments and units. The advertising has shifted to promoting the merits of “investing in apartments for rental return” rather than marketing to owner-occupiers. It appears the owner-occupier buyers have all dried up, perhaps they are among the 20,000 workers slated by the State Government for redundancies?

Or are potential owner-occupiers waiting for the release onto the market of thousands of houses and flats currently owned by State and Federal Government that are soon to be placed on the market as a result of the Government push for the private sector to provide (former) public housing by offering the tax-deduction carrot being offered to owners who place rental properties into the NRAS scheme?

One only has to attend the Home Show in Brisbane to see this over-night marketing shift or take a cursory glance at this Saturday’s Courier Mail Property insert. The marketing hype seems to have abandoned the (now) non-existent new owner-occupier buyers and switched to promoting the merits of “investing in units or apartments for rental return” since clearly, the notion of capital gain is now just a pipe dream, at least for the next 5-10 years.

Accompanying press releases and advertisements say how successful the developments are (or going to be – many haven’t even started building) and advertise the numerous sales that have already been made to “investors” for fabulous rental returns. Who is buying these apartments is the question. For example, one in Milton advertises that it has sold $90 million in pre-sales with a vacancy rate of 0.7% and a rental return of 12.4% p.a (Courier Mail Sat 21/7/2012) yet not a sod has been turned on the vacant site. Puzzling indeed.

Others are advertising rental returns of $600-$850 per week around Newstead and Bowen Hills yet a newly completed complex at Bowen Hills, just 2 minutes from the CBD has huge placards visible from the ICB offering rentals at $300 per week. Quite a difference from the advertised rentals of $600-$800 per week available to “investors” less than a kilometre away. Recent data shows around 130 apartments available for lease or sale in the Teneriffe and Newstead area. So while alleged hundreds of units are being “snapped up” by savvy investors cashing in on the “rental boom” (remember the mining boom?) around Brisbane, a number of large unit and/or apartment complexes have been abandoned before they even turned a sod. Puzzling indeed? Yet the marketers claim buyers are scrambling to line up and buy off the plan? More puzzling.

Tuesday, July 24, 2012

RBA's view

The RBA governor said future economic shocks that would hurt Australia could happen in a number of ways, such as a severe economic slowdown in China and a collapse in dwelling prices.

"The ingredients we would look for as signalling an imminent crash seem, if anything, less in evidence now than five years ago," he said.

"By the same token there are things we can do to improve our prospects or, if you will, to make a bit of our own future luck," he said. "Some of the adjustments we have been seeing, as awkward as they might seem, are actually strengthening resilience to possible future shocks. Higher more normal rates of household saving, a more sober attitude towards debt, a re-orientation of banks funding, and a period of dwelling prices not moving much come into this category," Mr Stevens said.

Read more: http://www.news.com.au/business/we-should-build-on-our-luck-rbas-stevens/story-e6frfm1i-1226433865255#ixzz21XBd1kh4

"The ingredients we would look for as signalling an imminent crash seem, if anything, less in evidence now than five years ago," he said.

"By the same token there are things we can do to improve our prospects or, if you will, to make a bit of our own future luck," he said. "Some of the adjustments we have been seeing, as awkward as they might seem, are actually strengthening resilience to possible future shocks. Higher more normal rates of household saving, a more sober attitude towards debt, a re-orientation of banks funding, and a period of dwelling prices not moving much come into this category," Mr Stevens said.

Read more: http://www.news.com.au/business/we-should-build-on-our-luck-rbas-stevens/story-e6frfm1i-1226433865255#ixzz21XBd1kh4

Oversupply of dwellings in Australia

"The 2011 Census revealed Australia had 7.8 million households, 900,000 lower than the NHSC’s figure, with population also growing by 300,000 less than previously estimated. These figures have come as such a shock that the NHSC chairman has reported that an undersupply could be incorrect. In fact, Morgan Stanley researchers have found that the current 228,000 dwelling undersupply has now become an oversupply of 341,000, a huge turnaround."

See: Don't be dudded by housing data

See: Don't be dudded by housing data

Sunday, July 22, 2012

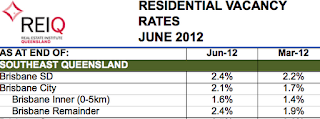

REIQ: "Rental demand remains strong"

Extracts from an REIQ Press Release from Friday 20 July 2012:

The Queensland rental market remained constricted at the midway point of 2012, according to the latest Real Estate Institute of Queensland’s residential rental vacancy rate survey. The REIQ June vacancy rates - compiled from surveying property managers from REIQ accredited agencies across Queensland - shows demand for rental properties is still exceeding supply in many parts of the State. As at the end of June, rental vacancy rates in many areas remained below 3 per cent, which is considered the equilibrium point of rental supply and demand.

“The first three months of the year are generally the busiest in the Queensland rental cycle so we often see vacancy rates particularly low during this period of time,” REIQ CEO Anton Kardash said. “What our latest survey shows us is that demand for rental property remained strong at the end of June with vacancy rates generally remaining tight. While we are seeing an increase in the number of first home buyers and investors in the sales market, their activity will take some time to flow through to the rental market, which should ease some of this pressure on supply and rents we are now experiencing.”

In Brisbane, the vacancy rate at the end of June was 2.1 per cent, a slight improvement on 1.7 per cent in

March. Inner Brisbane recorded a vacancy rate of 1.6 per cent in June, with property managers from

REIQ accredited agencies reporting some rent increases taking place, especially for houses, due to

stronger demand.

The Queensland rental market remained constricted at the midway point of 2012, according to the latest Real Estate Institute of Queensland’s residential rental vacancy rate survey. The REIQ June vacancy rates - compiled from surveying property managers from REIQ accredited agencies across Queensland - shows demand for rental properties is still exceeding supply in many parts of the State. As at the end of June, rental vacancy rates in many areas remained below 3 per cent, which is considered the equilibrium point of rental supply and demand.

“The first three months of the year are generally the busiest in the Queensland rental cycle so we often see vacancy rates particularly low during this period of time,” REIQ CEO Anton Kardash said. “What our latest survey shows us is that demand for rental property remained strong at the end of June with vacancy rates generally remaining tight. While we are seeing an increase in the number of first home buyers and investors in the sales market, their activity will take some time to flow through to the rental market, which should ease some of this pressure on supply and rents we are now experiencing.”

Hilton Gold Coast - Huge Number of Crashed Contracts

A number of years ago, I "awarded" the Hilton Residents on the Gold Coast as one of the worst apartment investments in SE Queensland. See prior posts. A number of years ago, there were many press releases about how successful the development was, and how many sales were made off the plan to investors. I could not figure out who was buying these apartments, or why, as this development was not in a prime location, and surrounded by vacant shops and topless bars.

Now it has come to light that many of the investors were from outside Australia, and more than 100 purchasers have failed to settle (or about 25% of buyers). Values have dropped dramatically, with apartments sold off the plan for $1.4M now valued at about $800,000. (This book would have been helpful to these buyers.)

A number of purchasers who did settle have not put their apartments into the onsite rental pool with Hilton, and offsite agents are making under the name "H Residences". This shows that rental returns are likely to be poor.

Many apartments on the Gold and Sunshine Coasts have decreased in value since 2008. I know of a recent Juniper beachfront apartment that was sold off the plan for over $1.4M, that remains unsold today at $800,000.

See also this article.

Now it has come to light that many of the investors were from outside Australia, and more than 100 purchasers have failed to settle (or about 25% of buyers). Values have dropped dramatically, with apartments sold off the plan for $1.4M now valued at about $800,000. (This book would have been helpful to these buyers.)

A number of purchasers who did settle have not put their apartments into the onsite rental pool with Hilton, and offsite agents are making under the name "H Residences". This shows that rental returns are likely to be poor.

Many apartments on the Gold and Sunshine Coasts have decreased in value since 2008. I know of a recent Juniper beachfront apartment that was sold off the plan for over $1.4M, that remains unsold today at $800,000.

See also this article.

Shrinking Apartment Sizes

In Brisbane, apartment sizes are shrinking. Newer apartments are smaller than older apartments. Many two bedroom apartments are now less than 85 sqm in total size (including balcony), compared with about 100 sqm five years ago, or 120 sqm ten years ago.

For example, DoubleOne3, a Devine project, has two bedroom, two bathroom apartments that have a total size of 74 sqm including balcony. The "Superior" two bedrooms, on the corners of the building are 105 sqm in total size.

As another example, the size of two bedroom apartments in Mirvac's Park development at Newstead range from 96sqm to 112 sqm. Mirvac builds larger than most developers, to a higher quality. But compare Mirvac's Quay West development in Brisbane from more than 10 years ago. There, the two bedroom apartments were 126 sqm. In Mirvac's Arbour on Grey, from about ten years ago, most of the the two bedrooms were around 109 sqm.

In NYC, the size of new rental apartments is also decreasing, but the size of owner-occupied condos is increasing. See NY Times. I think that a similar distinction will arise in Brisbane, where two bedroom apartments less than 95 sqm in total size will be relegated as investor only product. Moreover, care should be taken when comparing apartments. Often the smaller newer apartments are more expensive than the older, larger apartments.

For example, DoubleOne3, a Devine project, has two bedroom, two bathroom apartments that have a total size of 74 sqm including balcony. The "Superior" two bedrooms, on the corners of the building are 105 sqm in total size.

As another example, the size of two bedroom apartments in Mirvac's Park development at Newstead range from 96sqm to 112 sqm. Mirvac builds larger than most developers, to a higher quality. But compare Mirvac's Quay West development in Brisbane from more than 10 years ago. There, the two bedroom apartments were 126 sqm. In Mirvac's Arbour on Grey, from about ten years ago, most of the the two bedrooms were around 109 sqm.

In NYC, the size of new rental apartments is also decreasing, but the size of owner-occupied condos is increasing. See NY Times. I think that a similar distinction will arise in Brisbane, where two bedroom apartments less than 95 sqm in total size will be relegated as investor only product. Moreover, care should be taken when comparing apartments. Often the smaller newer apartments are more expensive than the older, larger apartments.

Saturday, July 21, 2012

Alex Perry Apartments - Sales Slow?

The developers of the delayed 11-storey Alex Perry Residential apartment block in Brisbane’s Fortitude Valley have removed all three-bedroom apartments from the design and are awaiting council approval on a modified development application. A spokesperson for developer Chrome Property told Property Observer there were few enquiries for the three-bedroom apartments since the project launched in May last year, complete with paparazzi and supermodels. The three-bedders have been replaced with one-bedroom apartments as part of a “redefined product”, and 77 of the 143 apartments will be sold to investors as serviced apartments with a hotel operator lined up to manage them. Investors are being offered 6% guaranteed rental returns for up five years net of management fees, with settlement anticipated for early 2014. Construction is expected to start at the end of the year, with completion in early 2014. One-bedroom apartments will start from $381,000 and two-bedroom units from $550,000. Chrome has been reluctant to reveal sales numbers since the project was launched.

Full Story Here.

Full Story Here.

Suburbs With Most Rental Properties

Brisbane Suburbs With Highest Proportion of Rental Properties:

- Bowen Hills

- The Valley

- Spring Hill

- South Brisbane

- Milton

- Kelvin Grove

- Kangaroo Point

- West End.

See detailed chart here and article from RP Data.

Friday, July 20, 2012

Q1 Trademark

A recent interesting Federal Court decision in favour of Mantra, that decides that the onsite manager can own a trademark for its letting business, even if the trademark is similar to the building name.

See Mantra IP Pty Ltd v Spagnuolo [2012] FCA 769 (19 July 2012):

"Like the Chifley Tower, “Q1” was a sign devised by Sunland, a private entity, to, among other things, signify or name its private building development. When it chose the sign “Q1”, it did not adopt or incorporate a geographical name such as that of an established town, suburb or district, like Surfers Paradise, or the Gold Coast. ... From this history, I do not consider there is any basis upon which any trader could claim to have any “common right of the public” to make honest use of the sign “Q1” as a trade mark. Put differently, there is nothing about the sign “Q1” that could be said to bring it within the “common heritage”..."

See Mantra IP Pty Ltd v Spagnuolo [2012] FCA 769 (19 July 2012):

"Like the Chifley Tower, “Q1” was a sign devised by Sunland, a private entity, to, among other things, signify or name its private building development. When it chose the sign “Q1”, it did not adopt or incorporate a geographical name such as that of an established town, suburb or district, like Surfers Paradise, or the Gold Coast. ... From this history, I do not consider there is any basis upon which any trader could claim to have any “common right of the public” to make honest use of the sign “Q1” as a trade mark. Put differently, there is nothing about the sign “Q1” that could be said to bring it within the “common heritage”..."

Wednesday, July 18, 2012

Residex Property Statistics June 2012

Residex has published its June 2012 statistics chart here. According to Residex, Brisbane apartment median valued decreased by 2.92% in the last financial year, and decreased just over 3% in the prior financial year. Melbourne was down over 4%. The number of sales of apartments in Brisbane increased slightly in this period.

Tuesday, July 17, 2012

South Bank Census Data

One area of Brisbane where there are many apartments is the South Bank area of South Brisbane. However, there is little data available about this area because it is leasehold land. The 2011 Census has some interesting data. The apartments in this area include Arbour on Grey, Saville Southbank (also known as Mantra Southbank) and Urbanest student accommodation.

- population - 804 people

- median age - 22

- Most people are in the 20 to 24 age group (31% of the population)

- 91 families

- 17% married

- 66% have University qualifications (compared with 13.5% for Qld or 14.35 for Australia as a whole).

- 231 dwellings in total (of which, 92% are apartments)

- Average of 2.1 people per household

- 66% of dwellings had 2 bedrooms

- Median weekly household income - $1,687

- 70% of dwellings are rented

- Median rent - $500 per week

- 0.9 cars per dwelling

- Ancestry: "The most common ancestries were English 17.2%, Chinese 16.1%, Australian 11.9%, Irish 5.0% and Scottish 4.7%."

- Country of birth: "In 3111003 (Statistical Area Level 1), 31.4% of people were born in Australia. The most common countries of birth were China (excludes SARs and Taiwan) 6.0%, Hong Kong (SAR of China) 4.9%, Singapore 4.4%, England 4.2% and Korea, Republic of (South) 4.0%."

- 68% had both parents born outside of Australia.

Monday, July 16, 2012

Brisbane City Census Data

For the past few weeks, I have been looking at the 2011 census data. It is very useful for property investors. In my view, the best place to search is via an address search, and the results are then available in layers, from a few blocks, to suburb, post code area, and so on. You can search here.

For Brisbane City downtown area, in 2011, here is some interesting data (full results here):

For Brisbane City downtown area, in 2011, here is some interesting data (full results here):

- population - 7,888 people

- median age - 29

- Most people are in the 25 to 29 age group (22% of the population)

- 1,526 families

- 32% married

- 37% have University qualifications (compared with 13.5% for Qld or 14.35 for Australia as a whole).

- 4,516 dwellings in total (of which, 98.7% are apartments)

- Average of 2 people per household

- 50.9% of dwellings had 2 bedrooms

- Median weekly household income - $1,828

- 54.5% of dwellings are rented

- Median rent - $530 per week

- 0.8 cars per dwelling

- Ancestry: "The most common ancestries in Brisbane City (State Suburbs) were English 18.0%, Australian 11.3%, Chinese 9.8%, Irish 7.0% and Korean 5.8%."

- Country of birth: "In Brisbane City (State Suburbs), 33.3% of people were born in Australia. The most common countries of birth were Korea, Republic of (South) 6.6%, England 4.4%, China (excludes SARs and Taiwan) 3.9%, Taiwan 3.3% and New Zealand 2.5%."

- 63.5% had both parents born outside of Australia

Sunday, July 15, 2012

Population Growth

Population growth often leads to property price growth. Statistics from the 2011 census were released recently, and show the population growth for Queensland. The question is whether this growth will continue, and at what rate.

The official population estimates show that Australia's population was a little under 4.5 million people in 1911 and by 2011 there were 22.3 million people.

The Commonwealth Censuses have also tracked the growth and development of the states and territories that make up the Commonwealth of Australia, as well as recording the distribution of the population between them. In the 100 years between 1911 and 2011, population growth for the two most populous states, New South Wales and Victoria, has largely tracked that of the national population. Both Western Australia and Queensland had relatively consistent shares of the national population until the 1960s and 1970s, when substantial expansion of the economies in both states began to occur, supported at least in part by mining development. Since 1911, Queensland's share of the national population has grown by 6.3 percentage points, while the population share for Western Australia grew by 4.1 percentage points.

See ABS

The official population estimates show that Australia's population was a little under 4.5 million people in 1911 and by 2011 there were 22.3 million people.

The Commonwealth Censuses have also tracked the growth and development of the states and territories that make up the Commonwealth of Australia, as well as recording the distribution of the population between them. In the 100 years between 1911 and 2011, population growth for the two most populous states, New South Wales and Victoria, has largely tracked that of the national population. Both Western Australia and Queensland had relatively consistent shares of the national population until the 1960s and 1970s, when substantial expansion of the economies in both states began to occur, supported at least in part by mining development. Since 1911, Queensland's share of the national population has grown by 6.3 percentage points, while the population share for Western Australia grew by 4.1 percentage points.

See ABS

Saturday, July 14, 2012

Brisbane Apartment property cycle improving: HTW

From HTW's month in review (July):

Brisbane Units as at June 2012:

Stage of property cycle: Start of recovery

Rental vacancy trend: Steady

Demand for new units: Soft

Trend in new unit construction: Steady

Volume of unit sales: Steady

This is the most optimistic that HTW has been in some time.

Brisbane Units as at June 2012:

Stage of property cycle: Start of recovery

Rental vacancy trend: Steady

Demand for new units: Soft

Trend in new unit construction: Steady

Volume of unit sales: Steady

This is the most optimistic that HTW has been in some time.

Friday, July 13, 2012

The most significant barrier to a housing market recovery

"The most significant barrier to a housing market recovery: 301,414 homes for sale.

The number of homes available for sale across Australia has been decreasing; however stock levels remain well above average. Over the four weeks to 8 July 2012 RP Data tracked 301,414 unique properties advertised for sale across the country. While the number of homes available for sale is very high, the volume has been reducing and is actually about -7.4% lower than when supply levels peaked last November. ... Clearly, the large number of homes available for sale is due to a lack of absorption rather than a large number of new listings being added to the market."

See Property Pulse.

There are also a large number of properties that owners want to sell, but cannot, so they have been withdrawn from the sale process and rented out, with the hope that the market improves.

The number of homes available for sale across Australia has been decreasing; however stock levels remain well above average. Over the four weeks to 8 July 2012 RP Data tracked 301,414 unique properties advertised for sale across the country. While the number of homes available for sale is very high, the volume has been reducing and is actually about -7.4% lower than when supply levels peaked last November. ... Clearly, the large number of homes available for sale is due to a lack of absorption rather than a large number of new listings being added to the market."

See Property Pulse.

There are also a large number of properties that owners want to sell, but cannot, so they have been withdrawn from the sale process and rented out, with the hope that the market improves.

Thursday, July 12, 2012

Subscribe to:

Posts (Atom)

{kind=link}

{kind=link}